New Politics and Economics

Trump’s new housing policy isn’t new but its effective.

This is a fresh newsletter, so fresh, the topic is yesterday’s announcement that President Trump has ordered Fannie Mae and Freddie Mac to purchase $200 billion in mortgage backed securities. This is what is known as quantitative easing a major economic policy move that will have the intended effect. It will lower interest rates and in the very short run, it will make housing more affordable for those who purchase in that window.

This isn’t new economic policy but it is unusual in that quantitative easing is typically carried out by the Federal Reserve and not the POTUS. More power to POTUS, this was necessary.

The economics lesson you didn’t ask for

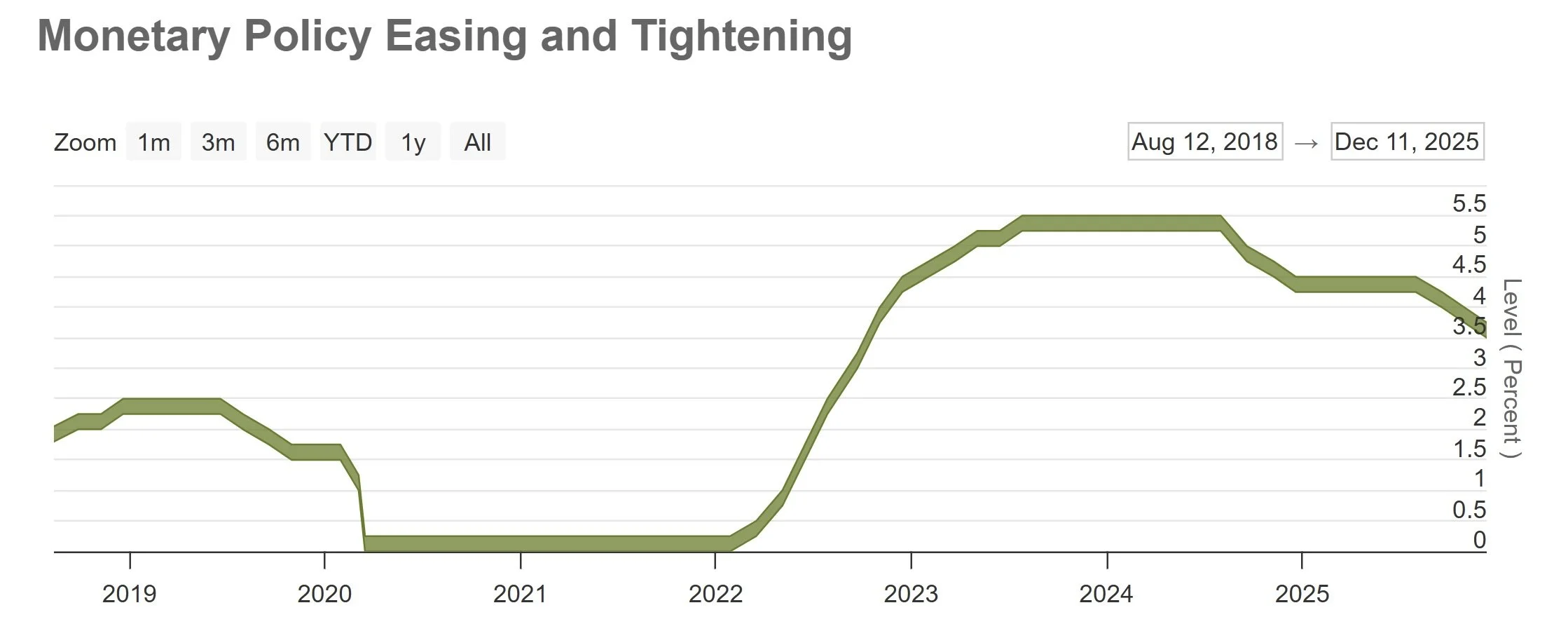

Quantitative easing is a way of injecting money into the economy to counteract a recession and encourage investment. To understand the Federal Reserve’s (FRB) power, think of the organization as a dam over a river and the river is the US economy. There is some optimal amount of water in that river at any given time, absent spontaneous and natural conditions. The U.S. Economy is that river and the water is the optimal amount of money supply flowing through it. The FRB is responsible for releasing money or tightening its flow into the economy to ensure there is an equilibrium in markets to achieve the dual mandate of low unemployment and targeted healthy inflation. For the last few years, the Federal Reserve has switched to a policy of quantitative tightening, reducing the flow of the money supply to cut off inflation. This followed their policy during Covid-19 of quantitative easing that hyper triggered the housing market and over time caused the inflation the subsequent tightening was meant to stop. Both actions had immediate impacts on the housing market, one hyper inflating it and the opposite and reciprocal response action sending it into recession. It is a delicate balance and often the FRB gets the timing wrong because of its limits.

If you want a shorthand of modern economic history: every artificial boom and bust in the United States economy in the last 40 years was caused or exacerbated by the Federal Reserve. I just saved you a whole semester of my macroeconomics class, my students are probably jealous. In my opinion, this FRB actually did an admirable job of keeping us out of an experience with deflation during Covid, it’s worse than inflation, I promise, and then froze in response to repeated red flags that housing had gone too far in the last 12-18 months.

Which brings me to the news of Trump’s executive branch policy; to be effective, the policy had to come from him. It was a bold, relatively unprecedented move that will have meaningfully positive short run impacts. The reason it had to be him is that the FRB moves at too slow of a pace to surprise markets and create quick responses in a positive direction. Due to the institutional structure of the FRB, and its unadvertised role of being the market whisperer, by the time they announce a policy shift, markets have already responded and the impact is a blip on the radar. When markets are stagnating or declining, they need a quick adrenaline punch and instead of waiting on the 535 across the street or the FRB, Trump put the adrenaline in.

This is probably not going to be the last housing stimulus of 2026 and given the pent up demand in the market from people who have sat out and waited, the next stimulus announcement will bring a new challenge for affordability. Think of the dam above the river, the first release of water may only put so many new buyers in the market and the market will absorb them at current prices. The next release brings in more competition and quickly puts upward pressure on housing prices, potentially swinging us from a buyer’s/neutral market back to a seller’s market. Congress usually doesn’t like to completely take a backseat to a POTUS in an election year so it wouldn’t surprise me to see fiscal stimulus to follow and some legislative work aimed at affordability ahead of the midterms.

Summary: This is a necessary infusion into the housing market and it will be effective. Many are bemoaning the short term nature of this move and talking about increasing housing stock and a bunch of other housing metrics like raising median incomes as real solutions. These are lofty goals and collectively, we should want those. But absent the country solving its collective action problem and politics suddenly becoming a system beholden to the 80 percent of Americans-those goals will only be accomplished by a thriving economy.

Think of this policy like giving a child ibuprofen to give them some relief during cold and flu season. You know it isn’t going to kill the virus or solve the root problem, but it will give them some relief so that they might heal and return to normal. Sometimes, the short run solution is just that, the best you can do to keep things moving forward. It might not fix everything, but it gets you on the road to recovery.

On the future of housing and the economy, this signals that the government is calling an end to the stagnant/declining pricing window of housing and it will likely have a quick demise. Fingers crossed, this might be followed by a normal market. If past is prologue, this normal market will be short lived and followed by another peak and valley. I would love to say it is a fool’s errand to predict how quick we overshoot normal again but it seems housing has been a ten year cycle for so long we might all have the power to be economists and fortune tellers.